Why I invested in Stripe at a ~$100 billion valuation

April 28, 2026

Stripe can be a great long-term investment if you want to bet on AI without betting on who wins AI.

TLDR:

- Stripe is the default payments provider for new startups, making it the default payments provider for AI companies

- All AI companies will need a way to accept payments regardless of who ends up “winning”, where value accrues (model vs apps), etc.

- Stripe’s founders are still driven, ambitious, and care about compounding the business over a 10+ year horizon and are reinvesting accordingly

- At ~$100B[1] it (was) the cheapest it’s been on a TPV basis in five years (and possibly since its inception)

I don’t have access to Stripe’s financials or any non-public info. Investing in a business without seeing their financials is a little crazy, but I think Stripe has the potential to be one of the best long-term compounders available today because of its position in the tech ecosystem & the growth of AI.

I was partly inspired by the thinking of of Munger/Buffett[2] and believe Stripe fits these criteria:

- It’s already a great business

- It will compound for 10+ years, helped by its role in supporting new & growing AI companies

- $100b valuation was justifiable

1) Is Stripe already a great business?

Stripe is the default 1st payment provider for most startups

Stripe is currently the de facto choice for startups accepting their first payments. My proxy for this is YC founders. Ask around “who’d you choose for payments?” and you’ll get looks of surprise. “...Stripe? Who else is there?”

IMO this is the single most important asset for Stripe to maintain & protect because everything else from their business flows from here.

Convincing companies to switch payment systems is far harder than getting them to pick you when they don’t yet accept payments. This is true even when you will clearly make them more money via e.g. less fraud. The switching costs are really high, and a big part of what makes many payments businesses valuable in the first place.

Given the clear value of being the “first” payment provider for startups, why don’t other large payment companies do it?

The issue is that the larger you become, the more you become a target for fraud and accidentally KYC’ing companies outside of your chosen risk profile. So what companies do instead is clamp down on their top of funnel, letting in only new customers that very clearly match their fraud and KYC risk profiles.

Stripe of course is also beholden to this issue. The difference is that Stripe just cares more. In the constant battle between providing an amazing onboarding experience for the marginal customer and making sure you don’t get eaten by fraud, Stripe simply says “why not do both?” Why not put in the work to maintain our beloved onboarding AND fight the fraud + KYC risk?

You don’t accidentally optimize for customers with literally $0 revenue over your current massive install base.

Stripe is of course not perfect, but they appear to have fought the good fight and will continue to do so. Sixteen years in it’s still easy to get started on Stripe.

You’ll know Stripe and its founders continue to care deeply about the company to the extent that getting setup on Stripe continues to be very easy & simple for startups.

Stripe is an index on the fastest growing companies in the world

Byrne Hobert says “index funds are, fundamentally, a bet that the cost of adverse selection from bad stock picks is lower than the cost of hiring someone to make good stock picks.”

So one way to think about Stripe’s business today is the positive selection bias of their customers.

Broadly speaking Stripe’s customers tend to be the most advanced & fastest growing companies in the world. They include all [3] of the Forbes AI 50 2025 and 80% of the Forbes Cloud 100.

Elad Gil has been calling this out for a long time, including back in 2020: “buying Stripe means buying an important subset of the internet.”

And that subset appears to be becoming higher quality & more valuable as AI continues to permeate the world.

Stripe has said “more new companies joined Stripe in 2025 than ever before… Businesses in the 2025 cohort grew around 50% faster than the 2024 cohort. The number of companies reaching $10 million ARR within 3 months of launch was double the 2024 count.”

And Patrick Collison added to that on a recent podcast that the 2026 cohort appears to be growing faster and bigger than the 2025 cohort.

This is the opposite of what you’d expect as companies get bigger: the best, most engaged, most profitable customers tend to sign up for things in the early years, not later. CAC tends to go up and retention down over time.

So Stripe seeing their customer quality improving appears to be a strong signal of the impact AI is having on their business.

Compared to its closest public competitor, Adyen, Stripe gets a better take rate and is growing faster

Because Stripe serves the long tail of startups and e-commerce stores, they have more pricing power than Adyen, whose primary customers tend to be large, worldwide enterprises. Stripe serves many of these customers too, but Adyen doesn’t have the startups.

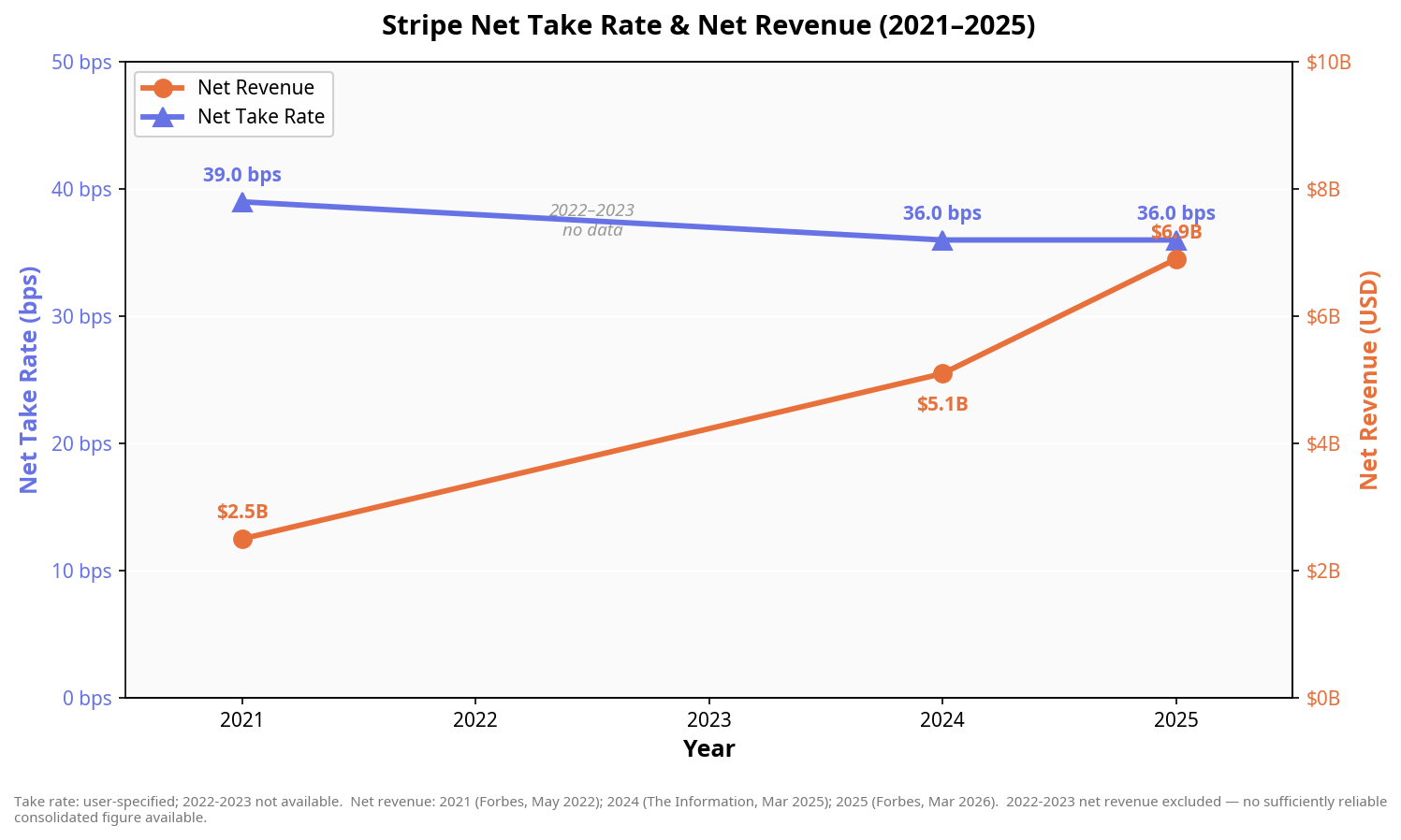

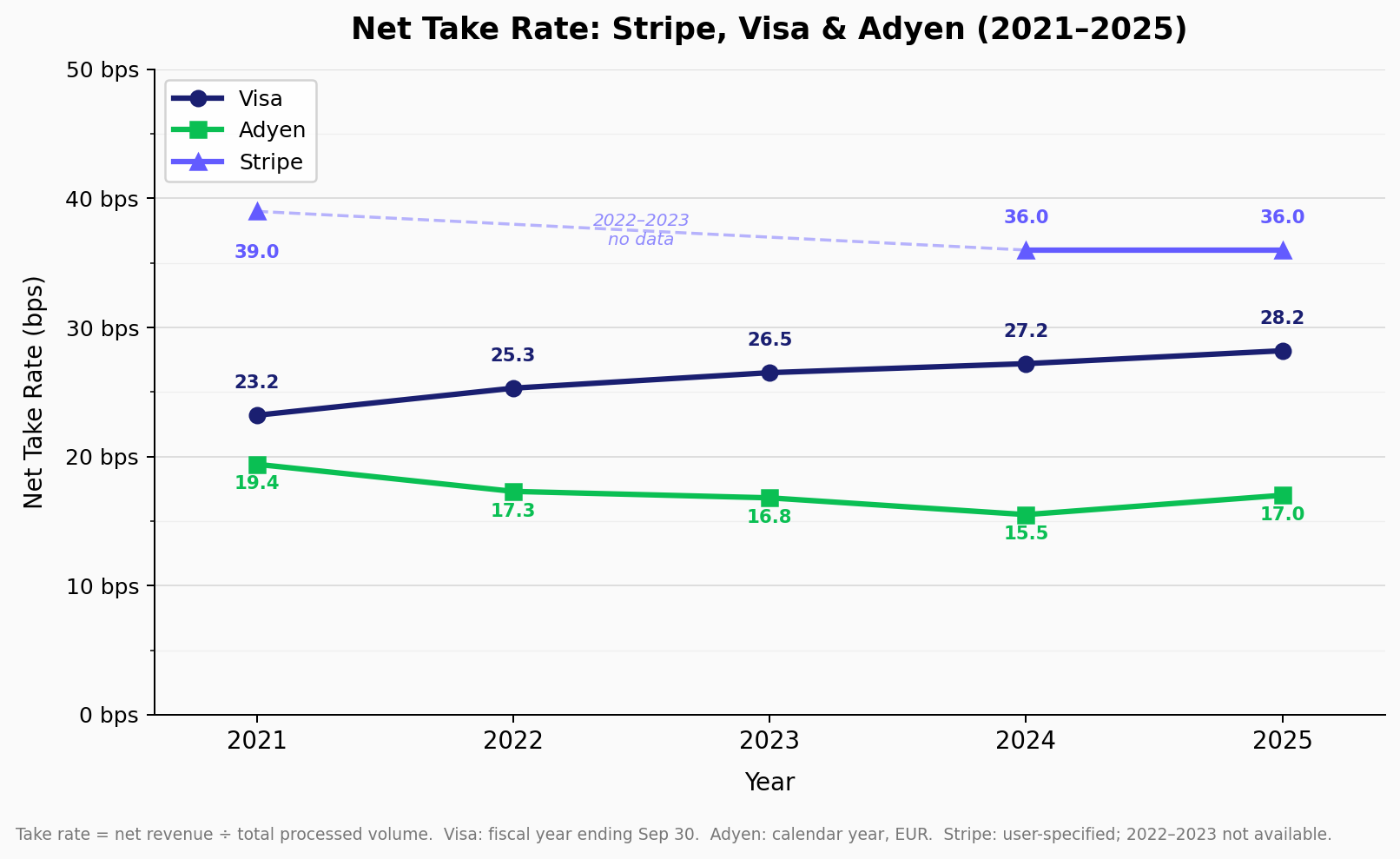

Stripe’s estimated net take rate in 2025 was 36 bps, while Adyen’s confirmed take rate was ~17 bps.

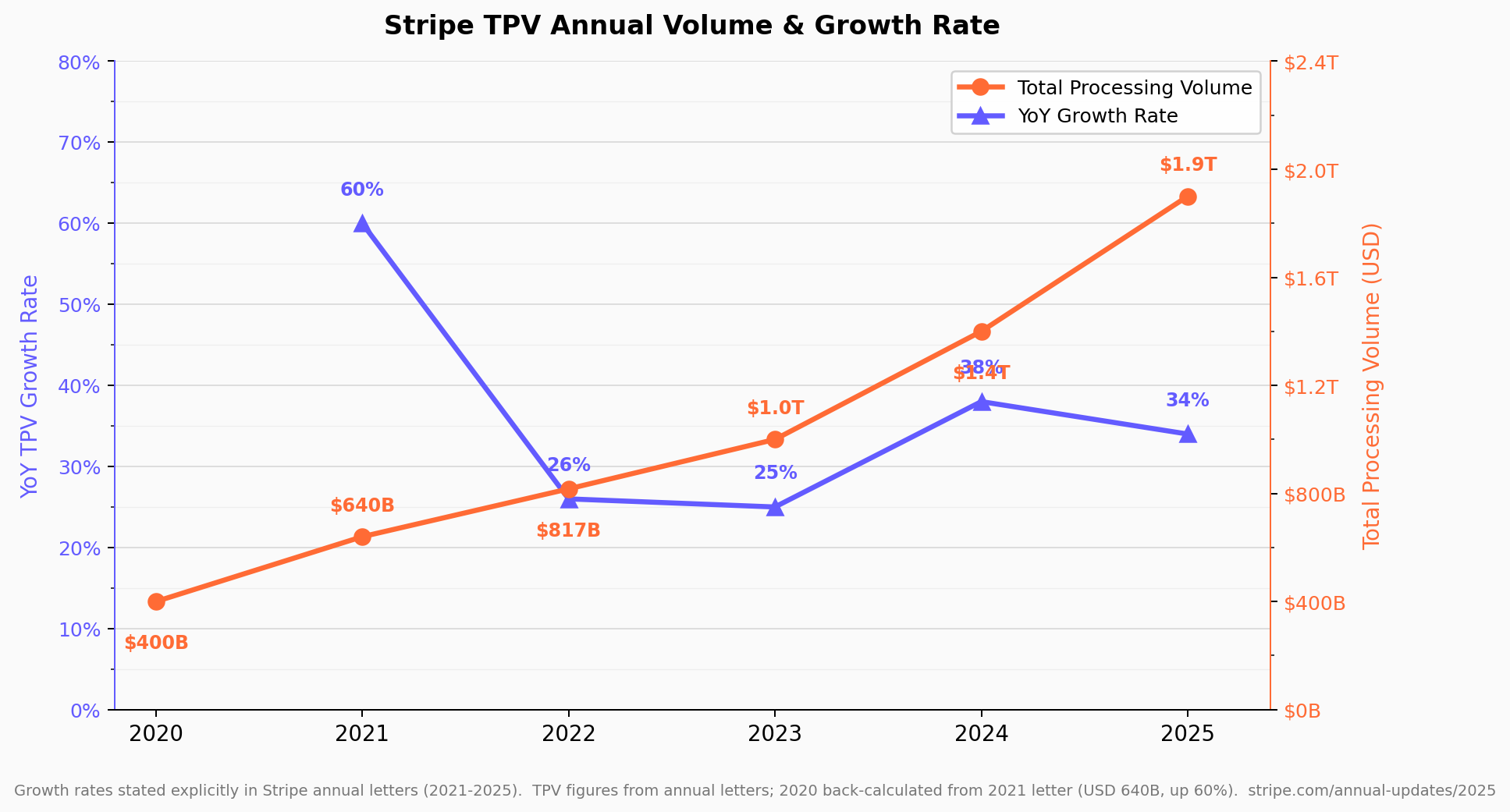

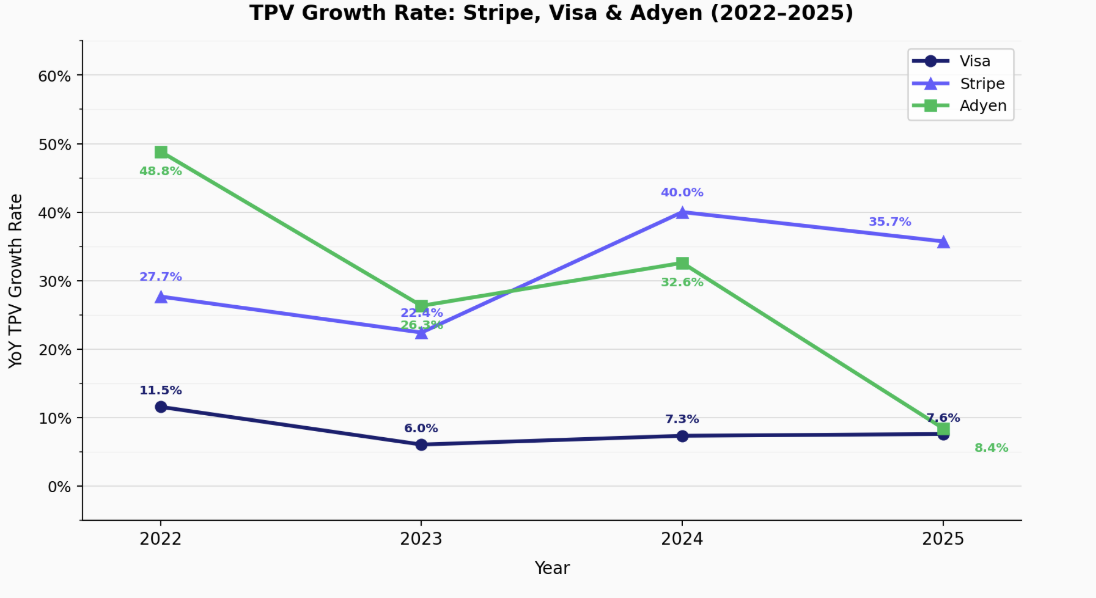

And for 2025 Stripe’s total processing volume (TPV) grew by 34% in 2025, while Adyen’s grew by only 8%.

The comparison to Adyen is important for at least 2 reasons: 1) take rate is probably the best available signal for whether Stripe has pricing power, and 2) because Adyen’s public we can rely on their market cap somewhat in trying to value Stripe.

Given the higher take rate and the higher growth rate of Stripe, Adyen’s market cap to me is the absolute floor to Stripe’s private valuation. [5] More on this below.

And some financial highlights

- TPV was $1.9 trillion in 2025 and $400 billion in 2020, meaning an annual compounded growth rate of the last 5 years of ~37%[6]

- Net Revenue was $6.9 billion in 2025 (source), up from $2.5 billion (source) in 2021, a CAGR of ~29%

2) Will Stripe Compound for a long time?

A “compounder” is a company that can achieve high returns on invested capital (ROIC) for many years.

I think one pattern that enables a company to have high ROIC for an extended period is:

- 1) a large or growing market, in order to have somewhere to invest the capital

- 2) a moat, so that earnings don’t get competed away allowing you to earn high rates of return, and

- 3) management that cares about allocating capital for the purpose of compounding the business

Let’s go through each of these 3 things

Stripe is building on top of a large & growing market with significant reinvestment opportunities that it is uniquely situated to make

“Payments” is an obviously large industry ($684 billion in worldwide revenue in 2024) that impacts and is affected by every industry & category in the economy.

So I note the large worldwide market for (possibly) adjacent reasons to why Stripe measures the % of global GDP running on Stripe (1.64200207% as I write this), which is to say that there is still a lot of market share[7] that Stripe stands to gain.

Inside that massive market some companies are growing quickly, some are growing slowly, and others are dying.

Which of those companies does Stripe tend to serve?

“The businesses on Stripe span every chromosome of the economic genome, from top corporate leaders (half of the Fortune 100 uses Stripe) to hyper-growth companies (we count 80% of the Forbes Cloud 100 and 78% of the Forbes AI 50 as customers) to newly formed upstarts (one in six new Delaware corporations incorporates with Stripe Atlas). At any scale, Stripe customers share one important characteristic: outsized growth. In aggregate, the revenue that businesses process on Stripe is growing seven times faster than that of all companies in the S&P 500.” - Source (emphasis mine)

It is still very early in the AI rollout

The previous quote was written over a year ago, when AI was definitely a thing but before Claude Code had launched. Claude Code’s release in Q4 of 2025 feels like a critical inflection point in the financial history of AI, in that the industry now appears to be accelerating, i.e. Stripe was already benefiting from AI before this recent acceleration.

And while the vibe certainly seems to be that AI is already huge, what’s more probable IMO is that it’s still quite early. Historical examples we can pattern match to include the iPhone and the Internet itself.

The iPhone launched in 2007, the App Store launched in 2008, and Uber launched on the iPhone in 2010. Benchmark didn’t invest in their Series A until 2011, almost 4 years after the iPhone was released. Instacart & Doordash weren’t started until 2012 & 2013, respectively. Doordash wasn’t started until 6 years after the iPhone came out. If the founding moment of the modern AI world is ChatGPT’s release in November 2022, then that means the Doordash’s of AI could start as late as 2028.

With the Internet 1995 was when it went mainstream with the release of Windows 95, Netscape’s IPO, and the AOL/Prodigy/Compuserve all allowing full Internet access. Looking back it doesn’t feel like the “real” Internet even existed before the iPhone, and yet anyone at home could sign up using Mosaic in 1993. And yet Facebook didn’t launch until 2004, a full decade later.

These things take time. It takes time for everyone to learn the lessons of the new platform/technology, internalize new assumptions and disregard old assumptions.

All of this to say: AI itself likely has a long, long way to grow. And all of this growth has to accept payments. [8]

Stripe is a bet on the intersection of AI & stablecoins

Perhaps less appreciated than the impact of AI is stablecoins. Because of the bad taste so many people have from “crypto”, stablecoins are still often written off as either useless at best or fraudulent at worst. That is just no longer the case.

Stablecoin transaction volume more than doubled in 2025 and is on track to double again in 2026. Newer companies like Arq, Felix, and Slash serve customers who rely on the existence of stablecoins to send & receive payments.

It’s tough to say where Stablecoins will end up in terms of importance and market impact. Will they become the default form of money and payments? It’s certainly within the distribution of possibilities. If money should be data, stablecoins are a solution hiding in plain sight.

The bear case is stablecoins turn into “just another rail” like FedNow. The two get compared because in theory they are both supposed to allow instant bank to bank transfers in the US.

But those qualifications (bank, and US) are precisely what distinguishes stablecoins from something like FedNow.

FedNow adoption requires entire financial institutions to opt in. With stablecoins you can send funds to anyone, anywhere in the entire world, instantly, with almost no 3rd party permissions required[9]. Only you and the recipient need to agree. This still appears to be underappreciated & undervalued, especially by people who bathe in the luxury of ubiquitous access to USD.

And with AI, stablecoins become a way to natively enable usage-based billing.

Stripe has a history of making high-quality long term investments, like Tempo, Atlas, Link, and Billing

I don’t want to just list everything Stripe is building. Instead I wanted to highlight a few different builts they’ve made:

Tempo

Tempo is a new blockchain built for payments, incubated by Stripe & Paradigm. Tempo has the opportunity to become the settlement layer for all payments denominated in stablecoins[10].

It does a few unique things:

- It is token agnostic and doesn’t have its own token, meaning it doesn’t prioritize or require anything to be done in a “Tempo” token

- That means as a user of Tempo you’re not bound to any single issuer. You can use any stablecoin to transact on Tempo, including one that you issue. And fees can also be paid in any USD-denominated stablecoin

- It has a dedicated payment lane for speed & fees, so if you’re e.g. sending payroll you know the payment will always be fast and always be reliably cheap

- And it has a built-in stablecoin converter, so 2 counterparties can send/receive in 2 different stablecoins cheaply w/o relying on external contracts or infrastructure

- All of this is done natively in the protocol itself

The point here is that Stripe would like to commoditize its complements. By decreasing the cost & friction of payments broadly and stablecoin transactions specifically, it will increase payment volume and in theory make more money. It doesn’t care about who wins stablecoins. It cares that it’s easy to transact in stablecoins.

Tempo barely went live with their mainnet in March. But they are already seeing large companies using it like Doordash. IMO Tempo is one of the most interesting things to happen in crypto.

Atlas

Atlas was launched in 2018 to help startups get incorporated faster and more easily. This includes things like filing your articles of incorporation, getting your EIN, and filing your 83b with the IRS.

As recently as a few years ago the revenue impact from Atlas was minimal. By definition, a company that started in 2018 as one of Atlas’s first users would only today, 8 years later, start showing material revenue for Stripe. Stripe said “we’re okay waiting 5-10 years for companies that use this brand new product to generate material revenues” and decided to build Atlas.

And they’ve also continued to improve and innovate on the product, which you can track yourself by following Stripe employees like Jeff Weinstein on Twitter.

And the investment in Atlas appears to be paying off.

Atlas now incorporates 1 in 5 of all Delaware C Corps, and 42% of Atlas C corps were AI companies. This large volume likely means Atlas is the single largest incorporator of AI startups in the world.

Cursor got started on Stripe Atlas. Would they have chosen Stripe for payments anyway? Probably. But given that Stripe’s most valuable asset is being the default payments provider for startups, it makes sense to find other ways to make using Stripe payments an even easier and more obvious choice.

Link

Link is Stripe’s consumer wallet that lets you store your payment credentials with Stripe and easily pay with any merchant who accepts Link. Stripe says it’s used by over 200 million people.

It’s becoming the best wallet for the Internet because of its convenience. As a consumer you get:

- All your payment credentials in one place, whether cards, banks, stablecoins, buy now pay later methods, etc.

- Payment credentials autocomplete with any merchant accepting Link

- Payment protection like you’re used to getting with your credit card (plus money back if you find a better price and reimbursement for return shipping and restocking fees)

- You can see all your subscriptions in one place in your Link profile

- And, my favorite, you can cancel your subscriptions from Link instead of having to go to the merchant. I’ve tried it, it’s super easy, and it works just like cancelling a subscription should work if you were designing for maximum convenience.

And yet even with 200 million people this product is still very early. So far Stripe seems to barely even market it to consumers other than via their merchant checkout pages. Link has an Instagram page with its first post in August 2025, and a Twitter account that was created in March 2025 (and the Twitter account appears to be targeting merchants, not consumers).

So if you really squint the traction Link has so far is kind of like if Cash App created 200 million accounts via only Square merchants instead of using massive advertising campaigns.

While I don’t think Stripe would ever say this publicly, in the fullness of time Link is likely a competitor to both the networks (V/MA) and Apple Pay. This is because it creates a closed loop, connecting the merchant relationships Stripe obviously already has to the new consumer relationships being built via Link.

It’s a huge opportunity, and one they’ve built quietly with little fanfare.

Billing & their Revenue Suite

Billing did $500m in annual revenue run rate as of February 2025. This is almost all margin, as the interchange costs for accepting the payment are already included in the payment itself. It’s part of their “Revenue suite” which is “on track to hit an annual run rate of $1 billion this year.”

This is especially good news because Billing has almost no net new marginal costs to Stripe. The card payment itself is already “covering” the interchange expense.

Stripe has a moat as long as it stays the preferred payments provider for new startups

Stripe’s most important moat is that it is the default choice of new startups to accept payments. Full stop. If it ever loses this, I will sell my shares.

But that begs the question of why is it the default choice? And how does it keep its position?

IMO what gives Stripe the right to stay the default choice and is their actual “moat” is they just plain care more.

They care about the details. They care about aesthetics. They care about speed. They care about doing as much work on payments infrastructure as possible so that the customer can ignore that entirely and focus on the unique aspects of their own business.

Patrick: “In as much as we have a moat, it’s because we have a very good understanding of our domain. We have a set of people who actually care about solving the problems, who are continually paranoid at the prospect that we might be forgetting something important.” - Source

Frankly Patrick himself doesn’t seem to even believe in moats. He believes in caring more: “For most products and most businesses, things can just be done much better. Moats are typically overrated.” - Source

It is this caring that, 16 years in, lets them open accounts for evermore diversified customer types and locations while still maintaining the “7 lines of code” install they’re famous for.

Are they perfect? Of course not. And the bigger they get the more complaints you will hear.[11]

But at least they seem to recognize who to prioritize. You have to care a lot 16 years in to keep fighting for amazing UX to serve non-existent companies.

And this moat gives them a few things:

First, because startups have the highest bar in choosing their vendors, it means Stripe’s product has to stay great to stay relevant. Serving startups is a way to make sure your product stays awesome. It needs to always be easy to get started on Stripe.

Second, because Stripe serves startups, it has a very long tail of customers in terms of customer size. And the smaller the customer, the less pricing power they have over their vendors. This means that Stripe gets better take rates relative to their comps like Adyen (more on this below).

This might seem counterintuitive: if startups have a high bar in choosing their vendors, and they can switch so easily, how does Stripe get better take rates?

This is because the incentive to switch when you’re smaller is small! You’re still focused on growing your business, not optimizing it. Reducing payment costs is an optimization function. When you’re smaller you’re still fighting to stay alive by finding product market fit and growing as fast as possible.

Third, it means their CAC is super low. [12] Again, they don’t have to convince startups to switch from another provider. Startups are already actively shopping for a payment provider, and the one they choose tends to be Stripe. [13]

Stripe is a bet on the growth of AI regardless of who “wins” AI

Whether the application layer or the model layer ends up accruing the most value, Stripe will be a beneficiary. Both Anthropic and OpenAI use Stripe to accept payments, and the long tail of applications using AI are also likely to use Stripe given its default, “why would I choose anything else” position in the tech ecosystem.

The likely biggest threat so far to Stripe’s leading position here was possibly usage-based billing. According to Patrick usage-based billing is the “native business model for the AI era”. And while I trust Stripe to build anything, usage-based billing with streaming events is a different architecture from subscriptions and discrete one-off purchases. Stripe made not 1, but 2 acquisitions to fill this gap, including the purchase of Metronome for a reported $1 billion.

While ideally Stripe would have built this natively themselves in a way that the market would have materially adopted them, it’s still a strong signal that they were able to move quickly enough to acquire Metronome to fill this hole.

Stripe’s cofounders appear to have the drive, vision, and desire to continue compounding

Patrick said to Forbes in 2022: “We’re not a glamorous business, just an infrastructure company that hopefully we’ll be able to compound for a long time.”

And John in 2025 in response to someone asking about when they’ll IPO:

“We’re not obsessed with the idea of particular financing events or capital events or anything like that. It’s not what drives us. We want to build really great products and great businesses and serve customers for a long time.” (emphasis mine)

I don’t want to do a hagiography of Patrick & John. But I will say this: they still appear to be fully invested in Stripe. Their ambitions have certainly not shrunk. If anything, I get the impression that they are just starting to harness their fully powered & operational battlestation.

Remember where they are: payments businesses at Stripe’s scale are incredibly profitable. Just look at PayPal. By most accounts the thing hasn’t been run well in over a decade, but it still spit out $5.6 billion in free cash flow in 2025 on net revenues of $33.2b. Stripe could absolutely coast and do the same if the lack of ambition & drive were absent.

Some anecdotes of their aliveness and what they’re optimizing for:

- Patrick still does customer interviews. He asks detailed, hyper specific questions. He still cares about the experience.[14]

- Acquisitions: Stripe acquired Bridge and Privy to jumpstart their stablecoins efforts

- Acquiring Metronome when they felt behind on usage-based billing [15] and/or needed to make a fast advancement for payments in the “native business model for the AI era”

- Their annual reports have been published earlier & earlier in the year:

- 2021: “April”

- 2022: April 5

- 2023: March 13

- 2024: February 27

- 2025: February 24

- The letter is published voluntarily, to the “Stripe community”, without any external entity pushing or requiring it. Why go faster? Why do this at all?

- Annual reports might seem like a trivial detail but this kind of thing only happens intentionally and if the top of the company cares about it

- You never get faster accidentally!

- The company continues to ship significant updates on their entire product suite.

- Incubating Tempo

- Creating the Agent Commerce Protocol with OpenAI

- Spinning up Stripe Projects almost on a whim after the success of Claude Code & Codex, to create an 10x better CLI UX to purchase & use online services

- And this is a year old but you can read their main updates announced at the 2025 Stripe Sessions conference here.

- John started a podcast where he does his own ad reads for Stripe’s services. What founder ~16 years into their massively successful company is like “hey you know what we need? A podcast to sell even more of our services”

- Patrick keeps a page on his personal website highlighting big projects done quickly.

They also invest more in R&D than any of their competitors. Why invest in the long term if you’re not building for the long term? Patrick & John don’t sound like people who want to spend their work & career time merely hanging out with unnecessarily compensated employees.

And they are in the IMO fortunate position of not needing to IPO. John again: “We have very much liked being able to do so as a private company because it allows us to focus on building the right products over a five or a 10-year time horizon.”

This is good on multiple levels.

First, it means the founders are not interested in doing fun things for only their appearance. It’s cool to go public[16]. It’s “fun” to go to the NYSE and ring the bell. Compounding year after year by making boring improvements to financial infrastructure is the least fun thing imaginable, yet this seems to be what drives the founders.

Second, as John notes it means the founders can take longer term bets without being punished by the public markets.

Third, it makes recruiting easier because your compensation isn’t subject to the volatility of your share price. When your share price is volatile and e.g. goes up significantly without being “earned” by fundamental changes to the business, you’re effectively rewarding current employees at the expense of future employees, hurting your ability to recruit.

Stripe’s reinvestment lens is long term and appears to have paid material dividends

In their 2024 annual letter Patrick & John said “In each of the last six years, Stripe has reinvested a much higher proportion of our earnings in R&D than any comparable company. We believe this ability will prove particularly important in the coming years, as stablecoins, AI, and other forces reshape the landscape. Stripe’s growth to date is evidence of the intense market demand for programmable financial services. The associated transformation is still early.”

One way to interpret this is thanks to AI, stablecoins, and other factors we believe there will be many new opportunities for Stripe arising in the near-, medium-, and distant-future We also believe that we are uniquely investing more in R&D to address these opportunities relative to our competitors and other payments companies.

See above section discussing Tempo, Atlas, Link, and Billing for examples of R&D investment in different cycles of payoff.

A note on ROIC (Returns on invested capital)

I don’t want to pretend a non-insider can calculate Stripe’s ROIC. The information to do this is not public. But there is where I lean on my analysis of the people and the available opportunities to reinvest.

3) Is ~$100 billion a reasonable price?

This is obviously tricky given they’re private.

But we do at least have Total Processing Volume (TPV) from Stripe itself every year since 2020. And TPV is the most comparable metric to other public payments companies like Adyen & Visa.

Stripe is growing faster than its comps

We can start by comparing TPV and TPV growth to other similar payment companies, Visa and Adyen:

Stripe is growing the most, and in the later years when their base is much higher.

It’s not super surprising that Visa isn’t growing, but it is a bit surprising that Adyen dropped off so much in 2025. They said it’s because of a single customer and that their growth would have been 21% instead of 8% but for a large customer (Cash App) but who cares? If your entire business is susceptible to a single large customer that’s also a sign that your business is less robust than Stripe.

Stripe has a better take rate than its comps

And crucial to payments companies of course is their take rate:

Stripe’s reported take rate is more than double Adyen’s. This makes sense: Stripe has a much longer tail of smaller customers who have less pricing leverage. Adyen is all enterprise which comes with lower pricing power.

Visa’s take rate is growing, which is impressive, though Stripe at least appears to have bottomed out.

As long as Stripe is both growing more quickly and has a higher take rate than Adyen, Adyen’s market cap seems to me to be an absolute floor on Stripe’s valuation. As I write this it’s roughly $36 billion, 22% of Stripe’s last public valuation two months ago. This is admittedly a large gap. I feel it is justified because I intend to hold for at least 5 years, and I think Stripe has made investments (see above) and is run by founders that are optimizing for the next decade plus.

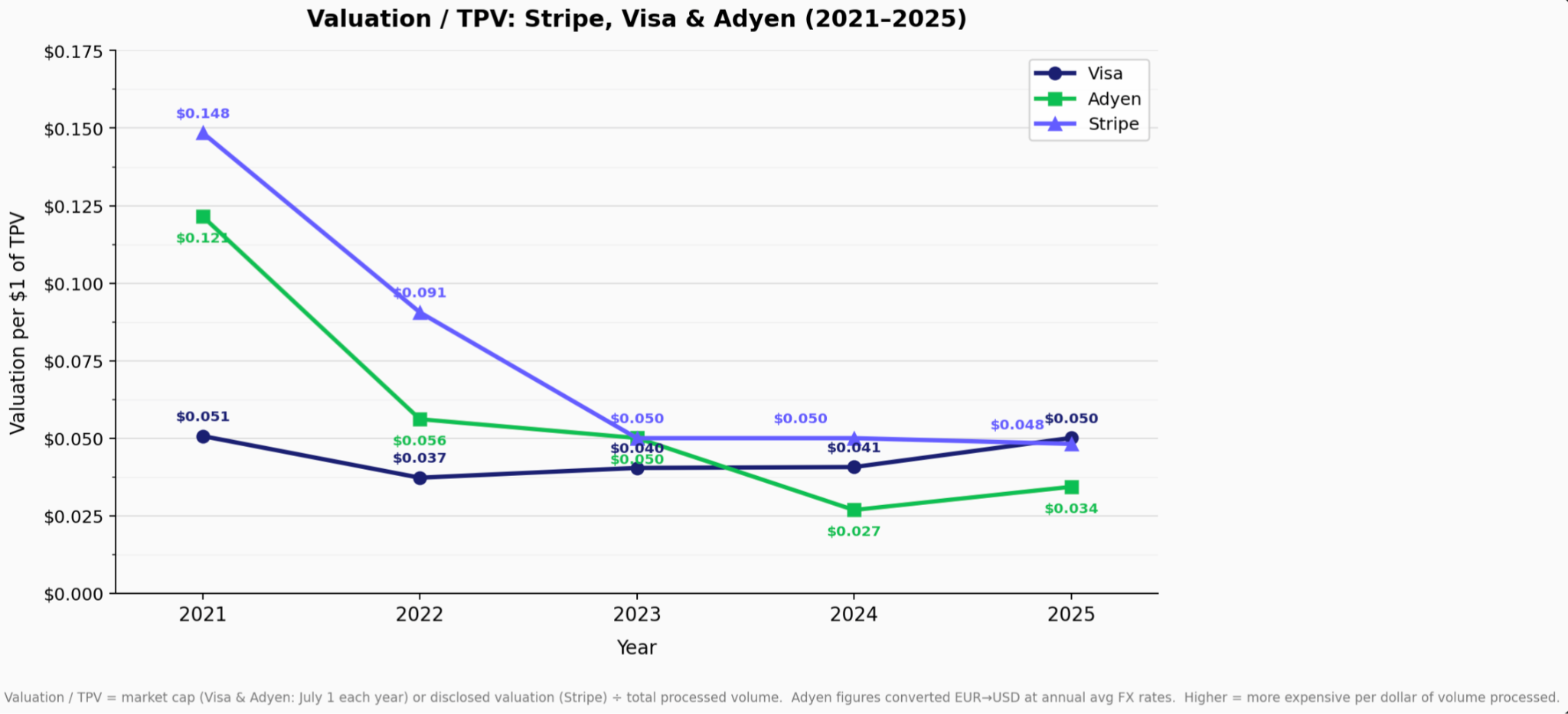

Relative to itself Stripe is the cheapest it’s been in 5 years (and possibly ever)

You can chart TPV to valuation ratios of payments companies to see how they change on a relative basis:

Looking at just Stripe itself, it’s become cheaper on a TPV basis over time. Its take rate has dropped slightly since 2021, but not nearly as much as the valuation / TPV rate. IMO this is at least partially due to Stripe’s share price going through more robust price discovery via secondary markets.

This doesn’t mean Stripe is cheap or expensive per se. But it does give us some confidence about whether and how much the private markets are inflating its price. It appears their valuation was significantly inflated in 2021, but that appears less true in 2025.

Bear cases – where could this go badly and where could I be wrong?

AI isn’t a huge deal

If you don’t believe AI will be the next important thing in tech then seeing Stripe compound at high rates of return for the next decade is harder to see.

Losing talent to AI companies

On the opposite end as AI has become hot I’ve heard from multiple Stripe ex/employees that people are leaving for AI companies. I don’t know how widespread this is, nor do I fully appreciate its impact on Stripe.

But it does recognize that Stripe is an old company by Silicon Valley standards (16 years), and it creates the question of whether Stripe will grow via momentum and the status quo, or whether Stripe will be able to continue creating differentiation and maintain their status as default payment provider of Silicon Valley.

How much do the founders care about dilution, stock-based compensation, and optimizing for shareholder returns?

This is possibly the scariest thing on the list. Technology companies are known for their high levels of stock-based compensation, and Stripe has to my knowledge never publicly disclosed theirs.

This is actually a subset for a bigger potential issue which is how much do the founders care about returns to shareholders? Is that something they’re optimizing for? Is it a nice but unimportant benefit of running a good business?

Stripe did change their equity vesting policy in 2021 to be 1 year for all new hires. Some more cynical takes said this was to decrease equity compensation.

Do private markets inflate prices?

I think that secondary markets have never been more liquid than today, i.e. prices for late stage companies, while potentially still inflated, have never been more exposed to price discovery than today.

Accredited investors can buy shares in many late stage private companies at e.g. Hiive, Equity Zen, Forge, or your local bulge bracket bank.

Hiive even gives their best estimate of the share price in a public page here, And you can see the price update on a daily basis and change rapidly as new information comes out. See also perpetual futures marketings like Ventuals.

And for the past 2 years at the same time as their annual letter Stripe has executed a tender offer to buy shares from employees/investors. This is capital from both investors and Stripe. I wouldn’t be surprised if this becomes an annual ritual, and Stripe shares are “officially” valued once a year according to the tender. This is one way the founders can provide a release valve to the constant interrogations about when they’re going to IPO.

One last point on Stripe’s private valuation: Stripe had been repriced down at least once. In 2023 they raised at a $50 billion valuation, almost half of their previously disclosed 2021 price of $95 billion.

What would make me strongly consider selling (in order of importance)

- Both founders seem less interested or both leave. Just one founder leaving would not worry me significantly.

- If another company becomes the clear default payment acceptance provider for startups

- This means something more fundamental has changed about the company. Either they’ve lost the will to be good at creating a great experience, they no longer care about startups, or they’re just too big and are no longer capable of doing longer-term important work.

- TPV growth falls below 15%

- This would mean the AI & stablecoin growth likely isn’t enough to carry the company into another decade+ of compounding

- Less important but still noteworthy: Shopify moving 100% off Stripe

Final Thoughts

Something I’ve learned multiple times in my own life (Bitcoin, startups generally, PE search funds) is that it is (usually) much, much earlier in a lifecycle than one realizes. We all have the bias of the information in our heads and the bias of our own experience. Those things tell us that a trend is happening, because we are by definition aware of it.

I feel the same way about Stripe. From the outside it’s felt like Stripe has “won” for a long time. But in my opinion that’s a bias. If we get to the point where money is the same as data and see the full fruition of Internet-native commerce and programmable money, we’ll look back on today as still very, very early.

Thank you to Shri Apte for reading drafts of this.

Not investment advice. For informational purposes only. Do your own research.

- $100b was not my actual purchase price as I cannot disclose it, but it was within 10% in either direction. It closed in Q2’25. ↩

- From Warren Buffett: “The blueprint [Munger] gave me was simple: Forget what you know about buying fair businesses at wonderful prices; instead, buy wonderful businesses at fair prices.” ↩

- As Stripe is keen to point out, it’s actually all of the AI 50 who have live products. At the time of Stripe’s writing, 11 were not yet live charging customers. ↩

- Which is good, because as I write this Adyen’s market cap is roughly 1/5 of Stripe’s latest private valuation

- Do Stadium Naming Rights Align With Shareholder Best Interests? ↩

- TPV is the single most important number for judging Stripe’s business because 1) its obvious correlation with revenue & general business performance, and 2) because it’s the only number that Stripe has reported on consistently, having done so every year since 2021. ↩

- I don’t think Patrick would ever talk about a business goal in terms of “market share” and I’m glad he doesn’t. But for our purposes I think it’s a concise & widely understood way of describing one way that Stripe can grow. ↩

- I didn’t want to bet on AI companies specifically. It feels too hard to pick the winners and losers. E.g. Google was assumed down and out of the entire AI race only a year and a half ago. And I thought about other obvious beneficiaries of broad AI adoption, like energy companies. But making a concentrated bet on a single or even a few energy companies also felt fraught. There’s no default energy provider to AI companies today, and the industry is quickly remapping itself to build supply as fast as possible to meet the new demand. Who seems to benefit no matter how AI grows, or who (in the US) builds it? The payments companies underneath. And who’s the best payments company? (And in looking for very broad exposure to AI I did also make a much smaller investment in TSMC. They feel so undermonetizied that people don’t even want to try to compete. I would have potentially dug in & invested more but the China risk feels too material.) ↩

- For the most seamless experience users will likely have to pass a KYC threshold, but 1) that is not required and 2) “supply is elastic” and so companies are building compliant ways to allow more people worldwide to pass KYC ↩

- And if you squint, what makes money look like data more than all payments being conducted in stablecoins? ↩

- This would be hard for me to deal with as a founder. If you look at percentages, your performance can be improving significantly. But with Stripe’s scale & volume you will still be hearing a LOT of complaints. At best this just hurts the vibes, but at worst it can lead you to do things that hurt the business. I am curious about how Patrick & John balance this. ↩

- A lot of readers will hate this but I don’t actually know their CAC numbers. But I do know it’s low because I started my own consumer payments business where we pulled this same move of targeting customers when they’re making their first vendor choice instead of trying to get them to switch (in our case it was serving immigrants choosing their first bank account upon arrival to the US. Our CAC was ~$1 USD for a funded bank account for a long time, which if you receive $500 or $1,000 sign up offers from big banks you know is extremely low) ↩

- Stripe has other moats, too, more typical of the Warren Buffett style (e.g. how does your business automatically get better as it grows) For example, when a card is used on Stripe, 92% of the time Stripe has already seen that card somewhere else. What that means is they can meaningfully reduce fraud in a way that new competitors cannot. ↩

- Based on a friend who was interviewed 1:1 by Patrick for this purpose ↩

- I’m speculating ↩

- Though Stripe staying private has certainly made going public slightly less cool ↩